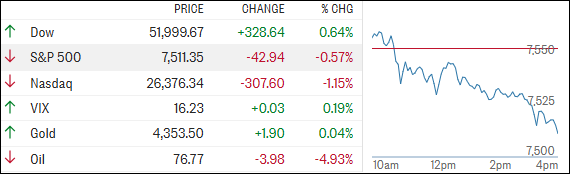

Market dynamics remain fragmented as SpaceX's post-IPO momentum continues to diverge sharply from broader equity trends. The 10% single-session advance reflects concentrated investor enthusiasm in aerospace and defense positioning, while the S&P 500 trades without directional conviction—a pattern suggesting selective risk appetite rather than systematic rotation.

The Dow's fresh record high, anchored by geopolitical optimism around potential U.S.–Iran negotiations, highlights the renewed valuation premium for economically sensitive sectors. Defensive positioning in large-cap indices masks underlying weakness in Technology, where profit-taking pressures offset the broader market's cautious optimism. Oil's decline reinforces expectations of stable-to-softer energy prices absent escalation scenarios.

This divergence—SpaceX strength against tech weakness and muted broad-market performance—signals investors are fragmenting capital allocation between growth narratives and cyclical reopening trades. The absence of coordinated sector movement indicates market participants remain uncertain about macro direction and policy implications from Iran negotiations.

Sector implication: Industrials and aerospace benefit from geopolitical deal flows, while Technology faces normalization pressures. Energy's weakness reflects demand concerns despite headline risk reduction. Volatility dispersion across sectors suggests elevated opportunity cost for concentrated bets absent additional catalysts.